Executive summary

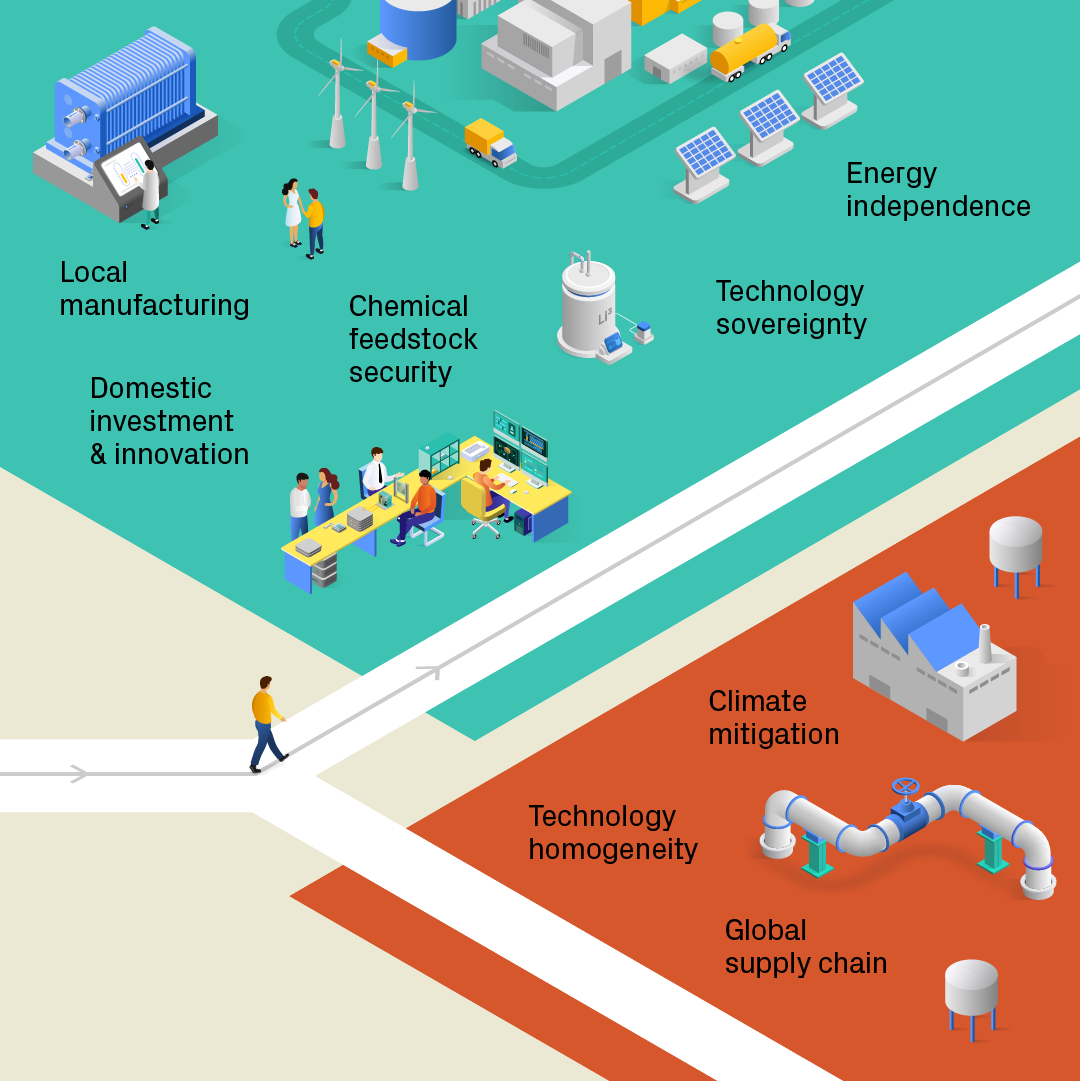

What was historically marketed as green innovation is undergoing a re-branding as secure, reliable domestic infrastructure and a drive towards reducing energy trade deficits. Funding continues to be allocated primarily into mature renewable energy & chemical processing infrastructure, but an increase in incentives for domestic production could force additional funding into more creative, earlier-stage technologies.

There is a positive development outlook for:

- grid-level energy storage technologies

- electrochemical processing for critical chemicals

- renewable power and accelerated grid infrastructure upgrades

- advanced nuclear and carbon capture

- synthetic (electrochemical) fuel processing

- mineral extraction

The reframing towards security should inprinciple improve investor sentiment by adding pragmatic justifications to the moral imperative of climate action. Technologies that tick multiple boxes – reducing emissions, enhancing energy & chemical self-sufficiency, and attracting investment will rise to the top. Purely climate-motivated initiatives that don’t clearly contribute to security might receive less attention and funding than before, as resources shift to the more tangible (and politically favourable) infrastructure of a secure energy economy.

Introduction

The global cleantech market is undergoing a shift in sentiment, language, and strategy. Technologies that were once promoted as tools to achieve net-zero emissions and combat climate change are increasingly being framed as instruments of energy security and independence. This trend is especially notable in major economies like the United States and Europe, where geopolitical unrest and supply chain disruptions have elevated the importance of domestic energy generation and chemical supplies. For instance, Russia’s invasion of Ukraine in 2022 triggered a scramble in Europe to replace Russian gas, recasting renewable energy and other clean solutions as means to ensure energy independence (REPowerEU). Indeed, it was a similar trend that saw unprecedented levels of government investment into solar and wind production in China, as the nation sought to rid its dependencies on Middle Eastern and Russian oil & gas and move towards a self-sustaining energy deficit. In the U.S., clean energy investments under the 2022 Inflation Reduction Act were justified not only for climate benefits but also for strengthening national energy security.

In this article, I summarise recent observations in the cleantech innovation world and examine how the narrative (and language) appears to be evolving in policy, technology development, and investment circles. I will give some suggestions as to how this rebranding might influence investment decisions, technology development roadmaps, and which technologies will rise in priority over the next 1–2 years as a consequence.

Rebranding net-zero technologies as tools for energy independence and chemical security

Recent shifts in energy policy narratives

In some Western economies, there is clear evidence that technologies traditionally marketed for decarbonisation are now being touted as crucial for energy security and even chemical security. In the last 2 months, the advice being given by (typically VC) investors to cleantech startups is to update their pitch material quickly to move away from “green leaves and trees” and towards national supply and security. This has mostly been sparked by the ongoing seismic changes in US politics. However, perhaps we already saw this coming. In the EU, the policy response to the 2022 energy crisis (sparked by the war in Ukraine) had already explicitly tied clean energy to national energy independence. The European Commission’s REPowerEU plan emphasises that “renewable energy is good for the climate, good for the EU’s energy independence, [and] good for the security of supply” (REPowerEU). Two years ago, this marked a rhetorical shift — wind, solar, and other renewables are no longer discussed only as climate solutions that are friendly to the environment, but as strategic assets to free Europe from volatile fossil fuel imports. Indeed, 2022 was the first year in which Europe generated more electricity from renewables than from natural gas, with 46% of EU electricity coming from renewable sources. EU leaders have highlighted this as a security milestone, noting that expanding domestic clean energy shields the bloc from external supply shocks. In addition, the EU accelerated its targets: the binding 2030 renewable energy goal was raised to 42.5% of overall consumption (from 32% previously) as part of its crisis response (independent of the climate-related objectives of the 2015 Paris agreement). These moves underscore how net-zero technologies are being reframed as the backbone of an energy-secure future.

Geopolitics and the move towards national chemical process security

The concept of chemical security has entered the lexicon alongside energy security, referring to secure supply of critical chemicals and fuels (I also like to include critical minerals here too). One example is ammonia (for fertiliser production etc.) and related chemicals. Traditionally, natural gas is a key feedstock for ammonia; Europe’s gas shortage has historically threatened fertiliser production, raising food security and pricing concerns. EU strategists now talk about reducing dependence not just on imported gas, but also on gas-derived products like fertiliser. A 2023 energy security report listed “ending European dependence on Russian energy-intensive imports such as oil products and fertilisers (ammonia, urea, phosphates)” as a top priority, and a dedicated task force was established by CEPA (Centre for European Policy Analysis) to manage the energy and process technology landscape.

At the start of 2023 nearly half of EU ammonia plants were still shut down due to the surge in gas prices - following the widespread curtailments in 2022. This crisis has prompted calls to invest in low-carbon domestic fertiliser production (i.e. green ammonia made from clean hydrogen) to ensure Europe’s food supply isn’t weaponised by foreign actors (Fertilizers Europe). Thus, technologies like green hydrogen – initially promoted to cut CO₂ emissions in industry – are now also framed as tools for strategic autonomy in chemicals. The European Commission’s new hydrogen strategy explicitly links climate goals with security, calling for 10 million tons of domestic clean hydrogen production by 2030 (and another 10 million tons of imports) “to reduce European dependence on Russian energy” while also meeting emissions targets (Hydrogen - European Commission). This example shows clearly how EU policy discourse post-2022 now firmly intertwines decarbonisation with the imperatives of energy and chemical security.

We have also seen developments in Morocco, where large portions of the world’s accessible phosphate reserves are found. These exciting developments are manifest in a drive for green fertiliser production via solar & wind-based electrolysis to generate green hydrogen, to be upgraded to ammonia and then to fertiliser. The “green” angle in this instance is indirect. Morocco has near ideal solar and wind conditions and little access to local oil or gas reserves. Therefore, the production of “green” ammonia is not only the most environmentally friendly approach to securing the countries supply to ammonia for fertiliser exports, it is also strategically the best from an energy/trade deficit and national independence perspective.

A re-framing of U.S. policy

In the United States, a parallel narrative shift is evident, driven by international competition and an industrial strategy that is trying to reduce the US’s trade deficit. The Inflation Reduction Act (IRA) of 2022, America’s landmark climate bill, was promoted as serving twin goals: fighting climate change and providing energy security. Roughly half of the IRA’s $369 billion in clean energy funding is explicitly dedicated to “the twin challenges of... climate change and energy security”. U.S. leaders increasingly cast clean tech in terms of energy independence – for example by reducing reliance on foreign oil through electric vehicles, or by building domestic supply chains for batteries and solar panels instead of importing them. In mid-2022, President Biden invoked the Defence Production Act to boost manufacturing of solar panels, heat pumps, insulation, and electrolysers, framing clean energy equipment as essential to national defence and grid resilience. A White House fact sheet described “today’s clean energy technologies” as a “critical part of the arsenal” needed to lower costs, reduce risks to the power grid, and address climate change (FACT SHEET: President Biden Takes Bold Executive Action to Spur Domestic Clean Energy Manufacturing). By using terms like “arsenal” and invoking wartime production powers, the administration signalled that renewables and efficiency technologies are no longer just environmental options but strategic necessities of an almost defence-like leaning. This link between clean tech and geopolitical strength suggests rebranding: solar panels and heat pumps are cast as tools to fortify the nation (much as oil or steel were in previous decades).

It’s worth noting that this reframing is not limited to government rhetoric — it reflects a broader convergence of motives in the energy transition. The International Energy Agency (IEA) observed in 2023 that “a powerful alignment” has formed between climate goals, energy security goals, and industrial strategies, all of which are now driving clean energy investment (Overview and key findings – World Energy Investment 2023 - IEA). In other words, what was recently marketed as green innovation is now also sold as secure, reliable domestic infrastructure. This change in narrative makes climate technologies palatable to a wider audience, when wielded effectively. In Europe, even countries previously hesitant about rapid decarbonisation embraced renewables as a way to escape Russian gas dependence. In the U.S., policymakers pitch clean tech as a way to out-compete China and create American jobs, which garners bipartisan support that pure climate arguments might not. The net result is that cleantech has been branded as a win-win: good for the planet, and good for national security and economic sovereignty.

Impacts of reframing on investment and technology development

Will the shift in framing from “net-zero” to “security and independence” have any impact on how these technologies are developed, funded, and deployed?

Increases in public funding and industrial policy

Well, to being with, major economies have already funnelled an increased amount of public funding into cleantech under the banner of energy security (Energy TransitionInvestment Trends - BloombergNEF). The EU’s REPowerEU program mobilised about €300 billion for clean energy and infrastructure to hasten the move away from Russian fuels (REPowerEU). These funds, drawn from EU budgets and recovery instruments, are accelerating renewable energy installations, grid upgrades, and cross-border interconnections. Similarly, the IRA in the U.S. has been designed to provide long-term tax credits for clean energy projects. At the time of its inception, the IRA was essentially intended as a decade-long market signal for investors to build renewable generation, batteries, hydrogen facilities, and more. By design, many of these incentives favoured domestic manufacturing and supply chains as a security measure. For example, the IRA’s credits for electric vehicles require domestically sourced batteries, and its renewable energy credits are higher for projects using U.S.-made steel and solar components. In Europe, the European Commission’s Green Deal Industrial Plan and the proposed Net-Zero Industry Act explicitly aim to scale up domestic manufacturing of clean technologies. The EU is targeting a scenario where 40% of its annual needs for key net-zero technologies are met by EU-based manufacturing by 2030, to “boost the competitiveness of EU industry, create quality jobs, and support the EU’s efforts to become energy independent.” (Net-Zero Industry Act - European Commission). This represents a strategic shift in development roadmaps: instead of purely global supply chains and lowest-cost procurement, there is new emphasis on local capacity, robustness, and control. A stark change from the feeling of inevitable globalisation in the 2000s!

Cleantech companies are adjusting their plans accordingly – for instance, multiple battery gigafactories and solar panel plants have been announced in Europe and North America, aligning with these incentives for local production. In short, the security framing has ushered in an era of active industrial policy for cleantech, with governments acting as catalysts and anchor customers (e.g. through procurement and subsidies) to accelerate technology deployment. While the West has some catching up to do regarding the skills and knowledge for manufacturing at scale – this changing mindset feels like the necessary first step.

A look back to cleantech investment over the last ~5 years

The types of investments flowing into clean energy are also evolving. On one hand, we see infrastructure and project finance taking a larger role, as some clean technologies mature from R&D concepts into deployable assets. Traditional venture capital investment in climate tech startups saw a dip during 2022–2023, partly due to broader market downturns – climate startup funding in 2023 was about 40% lower than the prior year amid rising interest rates and valuation corrections (State of Climate Tech 2023: Investment analysis). But at the same time, overall spending on deploying clean energy reached new records. Global clean energy investment was projected to hit $1.7 trillion in 2023, far outpacing fossil fuel investment (at about $1 trillion). In fact, for every $1 spent on fossil fuels, $1.7 was spent on clean energy in 2023 – a dramatic shift from a 1:1 ratio just five years earlier (Overview and key findings – World Energy Investment 2023 - IEA). Much of this growth is coming from large-scale projects: renewable power plants, grid expansions, energy storage installations, factory retooling, etc., often backed by corporate capital, government grants, or infrastructure funds (so not the “sexy” cleantech startups that come to mind for most people when talking about green technologies, but green technologies all the same). It is also the case that much of this large scale, mature sector investment is coming from China which accounted for over half of the overall global investment, and investing at almost twice the rate of any other country on a per GDP basis.

The alignment of energy security with clean tech has made institutional investors and utilities more confident in funding these big projects, since they now come with policy support, favourable economics (especially after 2022’s high fossil fuel prices), and public demand for stability (Overview and key findings – World Energy Investment 2023 - IEA). In other words, the narrative shift has de-risked certain investments: there is broad political will to keep funding and protecting domestic clean energy assets, which reduces regulatory uncertainty. While this has led globally to sustained investment in the deployment of mature clean technologies (solar, wind, battery manufacturing etc) this has not led to the increase in investment in earlier stage, higher risk technologies that many entrepreneurs have hoped for. So long as early-stage capital can generate high returns in software-heavy startups, the pitch for high risk, capital intensive technologies trying to displace established industrial processes remains challenging.

Changing investor sentiment and market incentives today

The reframing towards security should in principle improve investor sentiment by adding pragmatic justifications to the moral imperative of climate action. An increasing number of investors now view clean energy as a cornerstone of future economic resilience, not just a niche driven by environmental concern. As a result, market incentives are being realigned. For example, grid operators and regulators are recognising the value of energy storage and demand-side measures for reliability, leading to new revenue models for batteries (e.g. capacity payments or ancillary service contracts). The framing of cleantech as critical infrastructure has continued to encourage longer-term, lower-risk capital to enter the space – such as pension funds and sovereign funds.

One potential side effect of this shift is a degree of competition and protectionism in cleantech markets. As the U.S. and EU prioritise domestic capabilities, tensions have arisen (for example, European officials have been known to object to the “Made in USA” requirements of the IRA, seeing them as a threat to European manufacturers). This effect has only been exacerbated in recent weeks by the sudden shift in US trade tariffs. The security narrative, while accelerating investment, also means each bloc wants its own secure supply – leading to parallel incentive programs. This could fragment global markets somewhat, but it could also spur a “race to the top” where each region is trying to out-invest in technology (much as countries competed in oil & gas, aerospace, or semiconductor industries for security reasons in the past).

From an innovation standpoint, the infusion of funding and urgency is mostly positive: more projects and pilots are being backed than ever before (although the number of projects is still not as high as some might like).

Shifting Priorities: Which technologies are likely to benefit from the changing sentiment?

In the last couple of years, the cleantech domains that have gained higher priority reflect the lessons of recent crises and the demands of energy independence. Several technologies stand out especially, receiving more policy support and investment now than they did 1–2 years prior:

Grid-level energy storage

Ensuring a stable and flexible electricity supply has become paramount as renewable-based generation capacity rises. Large-scale batteries and other storage solutions are now seen as indispensable for energy security, providing backup capacity and grid stability when intermittent solar and wind outputs fluctuate. Both the U.S. and EU have elevated the role of storage. The U.S. Energy Information Administration reported record battery installations in 2024 (over 10 GW added) and expects 18 GW of new utility-scale storage in 2025 alone – a growth that highlights the importance of battery storage in balancing the grid. For the first time, storage is being built at scale alongside generation; in 2025, batteries and solar together account for 81% of new U.S. generating capacity additions (U.S. Energy Information Administration (EIA) ). This trend is driven by market incentives like the IRA’s investment tax credit for stand-alone storage and by reliability needs (preventing blackouts and managing peak demand). Europe, too, has recognised storage as critical – the EU’s Net-Zero Industry Act includes batteries and storage technologies as strategic net-zero technologies eligible for fast-tracked permitting and support (Net-Zero Industry Act - European Commission).

Overall, grid storage has moved from a niche pilot concept to a mainstream priority, propelled by the twin motives of integrating renewables and enhancing energy resilience. This will likely see healthy growth in technologies such as redox flow batteries, heat storage, and other forms of large scale/long duration energy storage.

Electrochemical processing for critical chemicals (H2, NH3…)

Among clean fuels, hydrogen has seen perhaps the largest jump (and fall?) in priority since 2020 due to its potential versatility in replacing natural gas, coal, and oil in various applications – and its role in chemical security (ammonia for fertilisers, refining, etc.). Pre-2022, hydrogen was often discussed in the context of long-term climate goals; now it plays an important role in industrial policy. The EU’s REPowerEU plan set a target to utilise 20 million tonnes of renewable (green) hydrogen by 2030 (half produced domestically, half imported), scaling up from its initial plans. This was a direct reaction to the gas crisis, aiming to use green hydrogen to decarbonise industry while also replacing Russian gas in sectors like fertiliser production and refining. To facilitate this, the EU is rolling out incentives such as carbon contracts for difference for hydrogen and accelerating approval of hydrogen infrastructure projects. In the U.S., the IRA created an attractive production tax credit (up to $3 per kg of clean hydrogen), sparking a wave of planned hydrogen projects as companies see a viable business case for the first time. However, many of these have still failed to materialise – the reasons for which should be the topic for another day.

Green ammonia, a derivative made from green hydrogen, has likewise climbed in importance: not only could it serve as a zero-carbon shipping fuel in the (longer term) future, but immediately it is a way to secure fertiliser supply chains. Countries like Germany are signing deals to import green ammonia from allies (e.g. from the Middle East & Morocco) as part of their energy security strategy, and are also exploring domestic production. However, like with green hydrogen systems, technical and financial challenges remain that have thus far hindered a real world deployment of purely green routes to hydrogen and ammonia being adopted at the large scale. Optimistically, rather than expecting another downward turn in the hydrogen market (as many will remember from the first hype cycle 20 years ago), there is a chance that the quickly evolving political climate will drive nations further towards scaling key infrastructure to secure their own supply of valuable chemical feedstock. Not as a “nice to have” but now as a “need to have”.

Renewable power and accelerated grid infrastructure upgrades

Traditional renewables – solar and wind – were already priorities for climate, but their strategic importance continues to grow. The need to reduce dependence on imported fuels led to an even faster build-out of renewables in the EU and a reinvigoration of renewables policy in the UK, U.S, China, and Middle East. For example, the EU in 2022–2023 streamlined permitting for wind and solar projects as an emergency measure, contributing to a record 96 GW of solar PV capacity installed in the EU in 2022 (REPowerEU). As a result, wind and solar together generated 22% of EU electricity in 2022, overtaking the share of gas for the first time (Europe Renewables in 2022 and 2023: Key Findings in 5 Charts). Governments have raised their ambitions: the UK’s Energy Security Strategy (2022) boosted offshore wind targets to achieve “greater energy independence” (The British Energy Security Strategy | Deloitte UK), and it created a body (Great British Nuclear) to drive new reactor projects (PM to put nuclear power at heart of UK 's energy strategy). The U.S. saw its largest-ever single-year additions of renewables in 2022 and 2023 aided by tax credits and by states’ policies, with solar and wind now often framed as homegrown energy reducing reliance on global commodity markets.

However, with this rapid scaling comes the recognition that grid infrastructure must be upgraded – a priority that has risen in tandem. Grid expansion and modernisation (new transmission lines, smart grids) are high on the agenda to ensure that renewable power can be delivered where needed and to avoid bottlenecks (World Economic Forum). Wind and solar are no longer viewed as merely climate-friendly options; they are the core of future energy security, and the focus has shifted to deploying them faster and integrating them via stronger grids and storage.

Advanced nuclear and carbon capture

Some technologies that had been contentious or on the sidelines have also seen their fortunes change recently due to security considerations. Nuclear power is a prime example: the energy crisis led multiple European countries to reconsider nuclear plant closures and even announce new projects, seeing nuclear as a firm, domestic source of electricity that can complement renewables. Again, what a shift from ~10 years ago! For instance, Belgium delayed the decommissioning of some reactors, and France doubled down on a proposal to build next-generation reactors as part of its drive for energy sovereignty. The UK’s strategy in 2022 put nuclear “at the heart of Britain’s energy security”, with a goal of 24 GW by 2050 (United Kingdom: The new Energy Security Strategy is launched). While nuclear remains primarily a climate mitigation tool, its framing is now often energy independence from gas and an attractive proposition (it seems) for energy-intensive data centres. However, the usual plague of heavy regulation around nuclear remains a large blocker and causes inevitable delays in real-world deployment, despite the promise and hype.

Likewise, carbon capture, utilisation, and storage (CCUS) has gained traction in the U.S. with enhanced IRA incentives ($85 per ton of CO₂ captured for storage) (IEA report). Though CCUS is about emissions, it also enables continued operation of domestic oil, gas, and industrial facilities with lower carbon impact – thus balancing climate goals with resource security (e.g. producing domestic oil with carbon capture, rather than importing oil). The EU’s Net-Zero Industry Act includes carbon capture in its list of strategic technologies (Net-Zero Industry Act - European Commission), indicating recognition that indigenous CCUS capability could support industrial security (keeping industries like steel and cement viable under carbon constraints). In the past two years, numerous CCUS projects have been proposed in North America and Europe, signalling rising priority.

Synthetic (electrochemical) fuels

Leading nicely on from CCUS, another area of increased emphasis is alternative fuels. Sustainable aviation fuels (SAF) and synthetic fuels for shipping have seen policy boosts (e.g. EU mandates for SAF blending) under the rationale of not being dependent on imported oil for transport in the future. These fuels were largely in R&D phase a couple years ago; now they are viewed through the prism of strategic reserves and supply diversification for the transport sector by the 2030s. We have seen an increase especially in novel electrochemical process pathways to convert captured carbon into value-add products. Thus, we see companies previously working on DAC and point source capturetechnologies moving up the value chain to electrochemical conversion.Similarly, we see traditional fuel manufactures moving down the value chain andresourcing development into catalyst and electrochemical systems.

Electrochemical material extraction

Finally, the topic of critical mineral security has been much discussed, particularly in the context of President Trump’s rhetoric regarding Canada, Greenland, and Ukraine. At the core of many energy & process technologies lie rare (read expensive) minerals, and nations are quickly realising that access to and extraction of these materials will be critical to energy security. As global demand for batteries and clean energy systems escalates, reliable access to high-purity lithium, nickel, cobalt, and other essential metals becomes paramount. Electrochemical processes could offer increased yield with lower environmental impact, enabling nations to reduce their reliance on imported minerals and thereby mitigate geopolitical risks. It will also enable nations with a sub-optimal natural reserve of such materials to extract them from lower quality sources. While the technologies capable of doing this remain at a low-ish TRL, the long-term benefits of establishing a development pipeline will help to boost the stability and resiliency of local supply chains. DLE is currently at the forefront of this – providing the ability to produce battery-grade lithium salts quicker than the traditional mining methods. However, similar technologies are also emerging to extract other valuable materials from sources such as waste chemical streams & tailings, or even uranium from the ocean (Nature, World Nuclear News)!

Overall, the prioritisation landscape in 2025+ reflects a convergence of climate action with security and industrial pragmatism. Grid stability solutions, domestic clean fuel production, accelerated renewable deployment, and end-use electrification are all on a fast track. The driving forces behind each are a mix of geopolitical concerns (e.g. reliance on hostile suppliers), technical needs (e.g. managing renewable intermittency), and proactive industrial policy (creating jobs and future-proof industries). Technologies that tick multiple boxes – reducing emissions, enhancing energy self-sufficiency, and attracting investment – will rise to the top. Purely climate-motivated initiatives that don’t clearly contribute to security (for example, certain nature-based solutions or international offsets) might receive less attention and funding than before, as resources shift to the more tangible infrastructure of a secure clean economy.

Conclusion and what to expect in 2025+

The evolving cleantech market shows how narratives and strategic framing will influence the trajectory of technology adoption. In the face of global upheavals - from wars to trade tariffs - major economies are reframing climate technologies as dual-purpose tools: they mitigate emissions while also strengthening national and regional security. Or rather, today they strengthen national and regional security while also mitigating emissions. This reframing is not merely semantic; it has unleashed concrete policy support and investment that accelerate the development and deployment of these technologies. In the U.S. and EU, what started as climate-driven innovation agendas have morphed into broad-based industrial transformations underpinned by the goals of energy independence, supply chain resilience, and economic opportunity.

This strategic shift in emphasis is likely to have lasting impacts. One optimistic outlook is that by broadening the appeal of cleantech (beyond environmental benefits to include jobs, stability, and national security), public and political support for the clean transition will be more robust. Investments in clean infrastructure may become less prone to rollback, since they will now be viewed as critical assets.

However, this new paradigm also raises new questions. Will the focus on domestic security lead to trade disputes or inefficiencies, as each region subsidises its own supply chains? Will the channels of investment for such technologies ultimately flow from defence budgets? Can the world ensure that a security-first approach remains compatible with global climate cooperation, rather than zero-sum thinking? These issues will require careful navigation.

For investors and innovators, the key will be to align with the strategic priorities driving policy: projects that address both emissions and resiliency will find support. For example, solutions for critical raw material recycling or substitution (to reduce import dependence on rare earths or lithium) might become as important as breakthrough battery chemistry itself. We will likely see climate tech companies increasingly branding their products in terms of reliability and security to tap into this sentiment.

The market’s evolution in the context of shifting sentiment demonstrates a blending of idealism and realism: the idealism of tackling climate change hand-in-hand with the realism of energy economics and geopolitics. Technologies once in the realm of environmental policy will now be placed at the heart of national security strategy. If managed wisely, it can create a virtuous cycle where security concerns drive more investment in cleantech, which in turn lowers costs and emissions, benefiting the entire planet, as originally intended.